How Rain’s Authorization Rate is One of the Highest Across Stablecoin Cards

Authorization rate is a direct measure of how well a card program’s infrastructure performs in the real world.

A high authorization rate means things like fraud checks, balance logic, and merchant codes are working as intended. A low authorization rate signals issues, like misaligned risk models, poor network compliance, or technical malfunctions.

Multiple parties are involved in approving or declining a transaction, but for the card issuer in particular, maintaining a high authorization rate is a significant lift. Fraud detection and network compliance are two of the biggest drivers of authorization rate, and both are Rain’s responsibility.

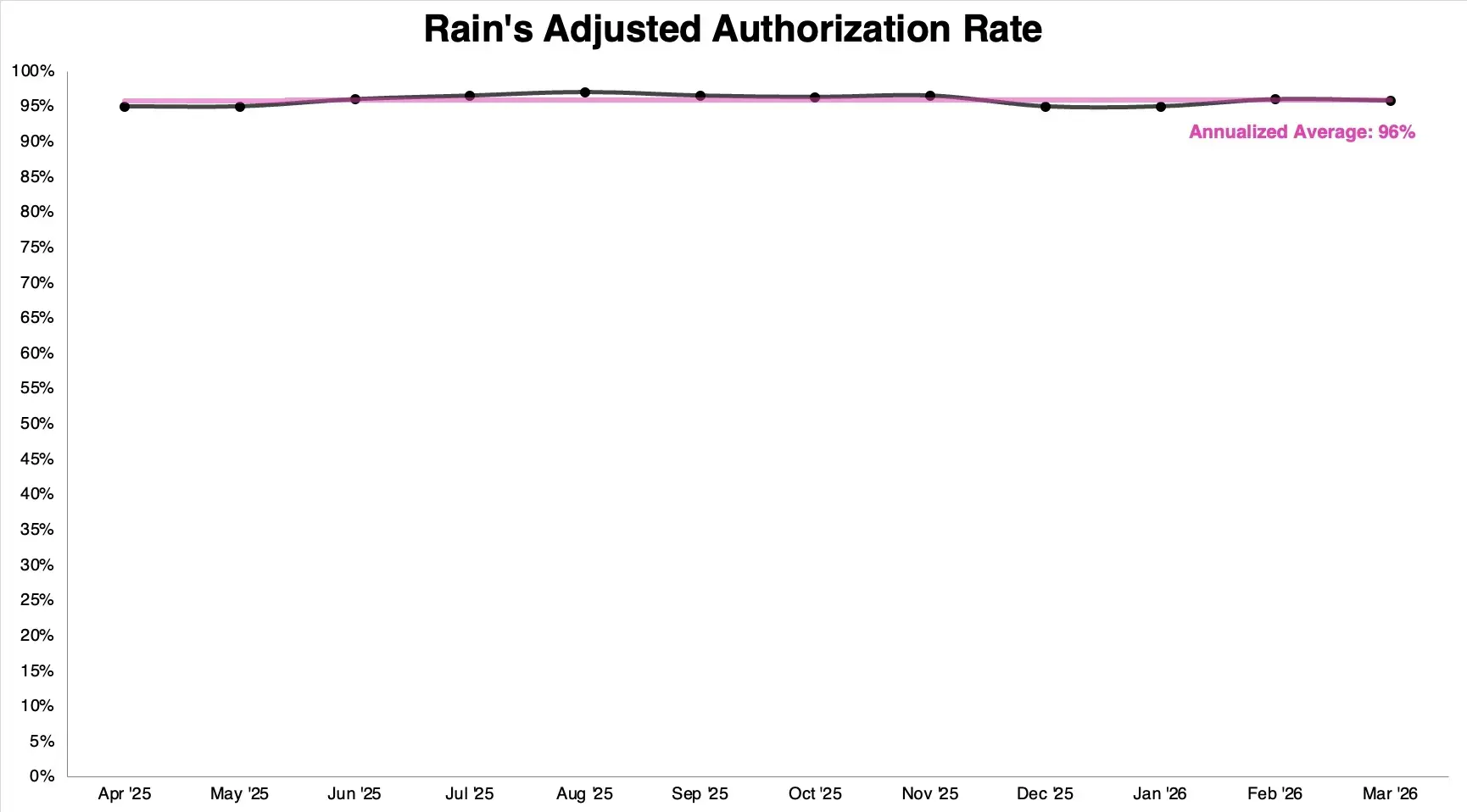

Over the past twelve months, Rain has consistently reported an authorization rate of 95% to 97%, excluding expected declines. This means when a cardholder makes an intended purchase with a Rain-issued card, it goes through nearly every time. The global average authorization rate is between 85% and 95%.

Rain’s authorization rate is the result of deliberate choices about infrastructure and risk management, choices we think every cardholder and partner should understand. Let’s explore:

Rain issues credit cards

One of the most significant variables impacting authorization rate is card product type.

Rain issues credit cards, an important differentiator from many other stablecoin-backed card programs, which typically issue debit or prepaid cards. This is a regulatory and network-level designation, and it matters because credit cards, as a category, consistently authorize at higher rates than debit or prepaid cards.

The reason credit transactions are approved at a higher rate is a combination of how networks route and handle credit, the compliance frameworks credit programs operate under, and how merchants and processors treat credit at the point of sale.

Rain’s design means most declines are expected

Card type is one factor. The other is how Rain's product is specifically structured, which impacts the nature of the declines that do occur.

Rain is a collateral-backed credit card, meaning every transaction is backed by secured assets. If a purchase amount exceeds the available deposits, the transaction is declined. As such, the vast majority of declines on Rain-issued cards are the result of insufficient funds. These are not systemic failures, but expected, mechanical outcomes that result from how the product works.

Partners have visibility into decline reasons through Rain's reporting, so if a transaction is blocked for this reason, they can alert cardholders. Partners can also build in notification tools that flag when a cardholder’s deposits dip below a certain threshold. These include push notifications, emails, or SMS to prompt cardholders to top up their balance.

Rain’s fraud detection is effective

A high authorization rate is typically indicative of a well-designed, functional fraud detection system. Overly aggressive fraud controls are not a sign that a program is safer, but an indication that the risk models lack sophistication.

A program that blocks liberally will inevitably block some fraud, but it will also block a significant volume of legitimate transactions. The fraud reduction is a byproduct of suppression rather than detection.

At Rain, the goal is not maximum blocking, it’s precision, and getting there starts early. A significant reason why Rain’s fraud detection program is so effective is that the due diligence process is extensive. Before a program goes live, Rain completes a thorough review of the partner's business model and risk profile.

At the cardholder level, Rain employs Customer Identification Program (CIP) standards that go beyond the regulatory minimum, collecting not just identity documents but information like occupation, annual income, and IP address. This additional context helps establish a baseline for what normal activity looks like for each cardholder, so genuinely unusual behavior stands out and declines are informed by real data, not indiscriminately issued. The result is a program that doesn't treat caution and performance as competing priorities.

The bottom line

Partners don't build card programs for the infrastructure, they build them for growth. More cardholders means more spend, which means more revenue. Authorization rate is one of the most direct levers for all three.

At 95–97%, Rain's programs are performing at the top of the market. Every percentage point above average is more transactions completed, more cardholders who keep using the card, and more revenue flowing to partners.

Rain's authorization rate didn't happen by accident, and it isn’t sustained without ongoing work. If you want to learn more about how Rain approaches card issuance or explore what a partnership looks like, let’s talk.